This article is part of the Futures in Long-termism series. You can read all other related blogs by following the links at the bottom of the text.

The clock is ticking, every second the world takes on more debt. Governments, companies and individuals around the globe are accumulating unprecedented loans, a trend that doesn’t seem to be reversing any time soon. Our economists and politicians are not persuaded about the societal costs of monetary deficit, and go as far as to say that Washington should end its debt obsession. On the other hand, deficit fundamentalists are arguing that it’s not long before we experience a full-blown debt crisis. But debt conceals a bigger disaster than just an economic downfall, debt eliminates possibilities for the long-term, consuming the future. Long Financing in a volatile world explores forms of investment that do not colonise the future.

Today, we’re witnessing the resurgence of an old phenomenon, Greece and Argentina have declared that their countries are becoming debt colonies in the face of austerity measures imposed by other nations. These new debt colonies formed through international loans and the ways in which sovereign debt and foreign direct investments work quickly become instruments of colonial subjugation. The latest IMF loan to Jamaica, a country that has been indebted for forty decades, is damaging its future by spending twice as much on debt repayments as it does on education and health combined.

This phenomenon extends beyond nation-to-nation borrowing. Since the financial crisis of 2008, the world’s companies, households and states have borrowed an extra $57 trillion, taking the global debt piles to an estimated 325 per cent of GDP. Eleven years after the financial crash our system is still being driven by the twin engines of rising debt and money creation by central banks. Each loan represents a claim on the future: that growth will always be positive in the future and thus we can use some of that value today. The problem is, that future may never exist. What happens when the time value of money evaporates? During an episode of the Keiser report titled Time No Longer Has a Price, Max Keiser suggests that ‘we live in a post-time, twilight zone of banking—like the bermuda triangle of banking. There aren’t enough assets (every single industry has been securitised and sold over 30–40 years) for liabilities’. We’re heading towards a secular stagnation—a condition in which there are poor growth prospects and no tools or investments to stimulate growth. As a result we’re consuming the resources and earnings of the future, today.

There are multiple risks in debt funds. In long-maturity debt funds, for example, volatility risks are higher as market movements have a higher impact on fund returns. According to Allianz Global Investors’ Autumn RiskMonitor survey, sovereign debt risk and volatility have topped the list of risks investors are worrying about. As debt continues to build up, Elizabeth Corley, CEO of AGI Europe, says: “We must now all admit that 2008–09 was not all of the Great Financial Crisis, but merely its opening act.” We are entering a period of increased volatility. That volatility is going to be amplified by the gargantuan debts staring down at us.

The future is called again and again to bail out the present. Jean Pisani-Ferry and Olivier Blanchard have urged central banks to finance a state giveaway by transferring thousands of Euros directly into the bank accounts of ordinary people to deal with the lack of monetary and fiscal stimulus options. Mario Draghi has backed calls for fiscal unions to bolster the eurozone and abandon austerity. The Positive Money movement is campaigning to establish a money and banking system that enables a fair, sustainable and democratic economy. How can we invest differently, without colonizing the future?

Experimental probe: OSLO investments

OSLO (Open, Smart, LOng) Investments attempt to combine the goods of two worlds—debt and equity. Debt investments grant companies the freedom to self-manage but rely on predictable futures and cannot tolerate volatility. On the other hand, equity is contingent on appreciating volatility but during the act of equity investment, company governance is diluted resulting in a diversification of strategic interests and decision-making processes, and creating Abstracted Organisations far removed from their context. This reality combined with accounting and fiscal tax bias (such as reporting periods, profitability, etc.) have created a future biased toward the short-term, and if exceptions for long-term investments are made, they’re predicated on the basis of significant predictability and rigidity—an ossified future.

Currently, we’re witnessing the design of alternative investments. For example, Blackrock’s New Circular Economy Fund engages public equities to take a bet on businesses that advance circular economy. Nesta’s Impact Investments focus on supporting innovations that help tackle major challenges facing older people, children and communities in the UK. And Evergreen Direct investments engage institutional investors to negotiate direct relationships with corporate management and form explicit requirements to build long-term environmental, social and governance values and parameters into enterprise capital investment processes. However these efforts still fail to address the way money is generated, loaned and what the implications are of these rigid future expectations.

Could we imagine new ways of financing projects that share the risk of investing conditioned upon multiple future outcomes and contexts, to be able to absorb volatility and de-colonise the future?

Precedents of investments that share some of these principles are convertible securities, these are types of investments that can be changed into another form. For example, convertible bond or debt is a hybrid security, which has the features of regular bonds—such as interest payments—but provides the possibility of conversion into a predetermined number of common stock or equity shares at a specific time, at the discretion of the bondholder. Islamic financing is another interesting field; since Islamic law prohibits the collection of interests payments, most financial instruments used in Islamic Banking are structured around revenue (and loss) sharing. However none of the above examples deal with systemic volatility—our current analogue systems require simple predictable returns.

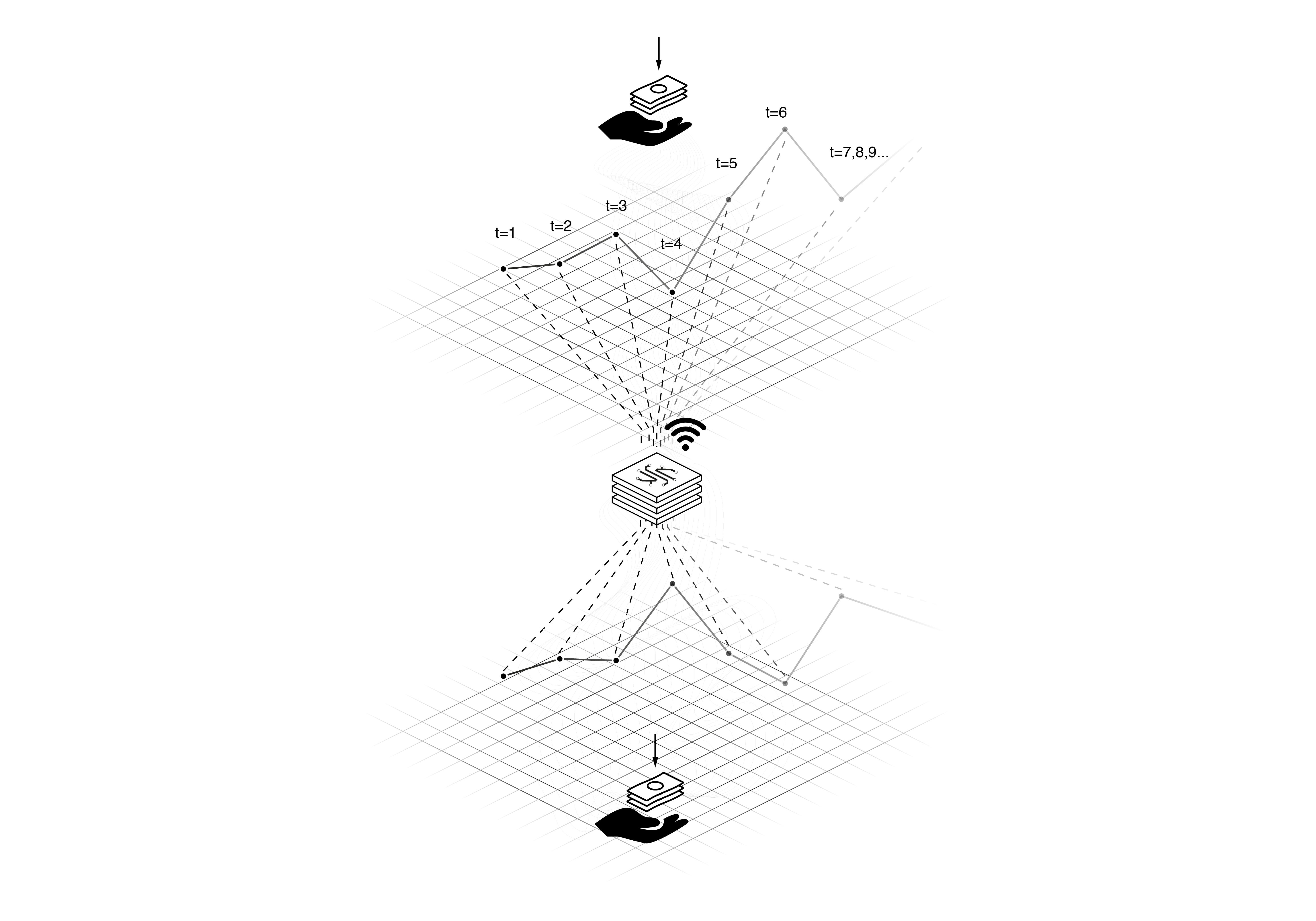

One trend this experimental probe could build upon is revenue-based financing in which payments to investors have a direct proportional relationship to how well a company is performing. An enterprise that raises capital through revenue-based financing will be required to make regular payments to pay down an investor’s principal. Interest is not paid on an outstanding balance, and there are no fixed payments. This is because payments vary based on the level of the business’s income. If sales fall off in one month, an investor will see his or her royalty payment reduced. Likewise, if the sales in the following month increase, payments to the investor for that month will also increase. Revenue-based financing is often considered as a hybrid between debt financing and equity financing.

A growing trend in revenue sharing is the use of smart contracts to act as a neutral third party overseeing transactions. Fully validated agreements happen in an instant using smart contracts, whereas traditionally parties would have to wait for weeks to fully confirm all transaction details. At the same time, smart contracts allow real time data updates that are fully confirmed, improving transaction saving accuracy dramatically. It’s here that we can start imagining long-term capital financing; investments that optimise for the long-term that are digitally autonomous—reducing bureaucratic costs—and responsive to real-time—reducing volatility costs, and as a result emancipating potential futures.

This experimental probe would explore a new generation of hybrid smart investment instruments—which are digitally Open (with the required transparency essential for governance), Smart (digital at source—essential to reduce the bureaucratic cost of contingent, real-world financing), Long (structured long-term agreements which are contingent on future contexts):OSLO Instruments.

This is one of another six interdependent experimental zones and probes we’re investigating as part of our work on Futures in Long-termism.

You can read more here:

1. Perishable Selves to Persistent Selves

2. Obsolete Objects to Persistent Things

3. Abstracted to Entangled Organisations

4. Shrinking State Care to Long Welfare

5. Short-term Investments to Long Financing in a volatile world

6. Limited Representative Democracies to Long Democracies

These pieces have been co-authored by Chloe Treger, Indy Johar and Konstantina Koulouri. The visuals were developed by Juhee Hahm and Hyojeong Lee.

This portfolio of experimental probes is part of broader system of interventions being prototyped by the Long Term Alliance.

The Long Term Alliance is co-founded by EIT Climate KIC, Dark Matter and a cohort of partners focused on five Areas of Action, which when combined seek to leverage systemic impact—changing behaviour, mindsets and action towards a long-term oriented society.

Our five Areas of Action are: Resetting the Rules of the Game for Regulation and Governance; Rethinking Notions of Value to Reform the Financial System; Empowering Individuals through Information Transparency, Capability Building & Behaviour Change; Enabling Collective Action & Creating New Democratic Spaces to Create the Ground Swell Pressure for Change; and Shifting Culture & Narratives to Promote Long-Term Mindsets.

In parallel and in recognition of the scale of change necessary, EIT Climate KIC together with Dark Matter and our partners are also experimenting with new instruments, mechanisms and vehicles that can invest over longer time frames, invest in the institutional deep code experimentation necessary, invest vertically in portfolios spanning deep culture change to new institutional infrastructures to accelerate the transition of Europe towards a long-term society.